An insurance rejection letter is written to sound like a verdict. It is actually an opening position, and July 2026 supplied the proof: the NCDRC ordered HDFC Life to pay a ₹75 lakh life insurance claim it had repudiated, because of one provision the insurer could not argue around, Section 45 of the Insurance Act, 1938: once a life policy has run for three years, it cannot be called in question on any ground whatsoever. The same week, a court hearing a mediclaim dispute observed acidly that insurers can appear more interested in premiums than in claims. This guide is the complete playbook for a rejected claim: what Section 45 actually says and the traps inside it, the six-step escalation from grievance cell to IRDAI's Bima Bharosa to the Insurance Ombudsman to the consumer commission, the special rules for health-policy rejections, and the documentation habits that decide these fights before they begin.

Key takeaway: families abandon lakhs every year because a repudiation letter sounds final. It is the start of a process, not the end of one, and the process is stacked with free forums: the insurer's own grievance cell, the regulator's portal, and an Ombudsman whose award binds the insurer up to ₹50 lakh. Escalate with records, not adjectives.

Section 45: the three-year rule that ends most arguments

As substituted in 2015, Section 45 draws one of the brightest lines in Indian financial law:

- After three years, counted from the later of the date of issuance of the policy, the commencement of risk, the revival of the policy, or the addition of a rider, a life insurance policy cannot be called in question on any ground whatsoever. Not misstatement, not non-disclosure, not even alleged fraud.

- Within the first three years, a policy can be questioned on the ground of fraud, or of misstatement/suppression of a material fact, but the insurer carries the burden: it must communicate the specific grounds and materials to the policyholder or nominee, and mere non-disclosure without materiality and intent does not qualify. Where repudiation is for non-fraudulent misstatement, the premiums collected must be refunded.

Parliament wrote the rule to end a specific abuse: insurers collecting premiums for years without question, then investigating only when the claim arrived, mining the proposal form for an undisclosed clinic visit from a decade earlier. Section 45 forces underwriting scrutiny to the start of the relationship, where it belongs. The July 2026 NCDRC order is the provision working exactly as designed: the policy had run its three years, and the "concealment" defence died on the date arithmetic alone.

The two traps hiding inside the three-year clock

- Revival restarts the clock. A lapsed policy that is revived gives the insurer a fresh three-year window from the revival date. The practical rule: keep premiums regular; a lapse-and-revive cycle is not just an administrative event, it re-arms the repudiation power.

- The proposal form is everything within the window. Most repudiations are built from a form an agent filled in a hurry while the customer signed at the flagged boxes. Fill the form yourself, disclose generously (illnesses, habits, other policies, occupation), and keep a copy. Over-disclosure costs a slightly higher premium; under-disclosure costs the claim.

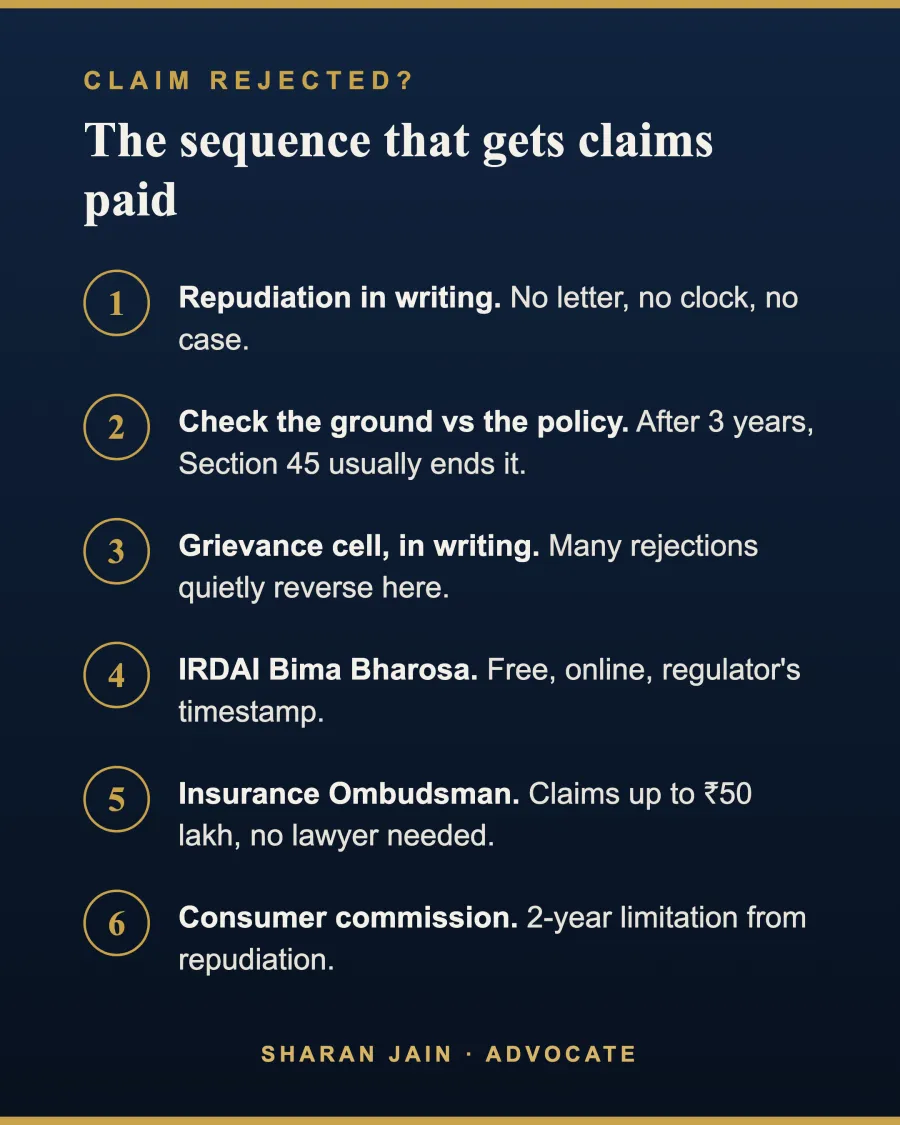

The six-step escalation ladder

| Step | Forum | Cost / time | What it achieves |

|---|---|---|---|

| 1 | Written repudiation with reasons | Immediate | No letter, no clock, no case. Insist on it; oral rejections are stalling |

| 2 | Policy-vs-ground check | A careful evening | Waiting periods, defined exclusions and Section 45 dispose of many rejections on paper |

| 3 | Insurer's Grievance Redressal Officer | Free; ~15 days | A surprising share of wrongful rejections quietly reverse here |

| 4 | IRDAI Bima Bharosa portal | Free; online | Puts the regulator's timestamp on the dispute; insurers respond on the record |

| 5 | Insurance Ombudsman (claims up to ₹50 lakh) | Free; months, not years | Award binds the insurer; policyholder stays free to litigate if unhappy |

| 6 | Consumer commission | Nil fee up to ₹5 lakh claims; 2-year limitation | Compensation beyond the claim: interest, harassment, costs; the ₹75 lakh order came from this track |

Sequence matters for two reasons. The Ombudsman expects the insurer's grievance process to have been tried first (or a month to have passed without reply), and complaints to the Ombudsman should come within a year of the insurer's final reply. And every written round you complete builds the record the later forum reads first. The consumer-commission mechanics, forum by claim value, e-Daakhil filing, evidence, are covered in our standing guide to filing a consumer complaint in India.

Health insurance rejections: the special battleground

Mediclaim repudiations lean on a small set of recurring grounds, each with a counter the policyholder should know:

- "Pre-existing disease" (PED): the term has a defined, regulation-bound meaning, broadly, a condition diagnosed or treated within the 36 months before the policy, and PED exclusions themselves expire after the regulator-prescribed waiting period (at most 36 months of continuous coverage under current health regulations). An insurer cannot stretch "PED" to cover every ailment with a hindsight connection to something old; commissions test whether the condition was actually diagnosed, actually material, and actually concealed.

- Waiting periods and specific exclusions must be in the policy words and were required to be disclosed at sale; ambiguity is read against the drafter, the insurer, under the contra proferentem principle.

- Moratorium: under the health regulations, after the prescribed years of continuous coverage (60 months under the current framework), claims cannot be contested on non-disclosure grounds except proven fraud, health insurance's cousin of Section 45.

- Portability: continuity earned with one insurer carries to another; a ported policy is not a fresh three-year window for PED arguments where the regulations preserve continuity.

The July mediclaim matter in the news, where the court rebuked the insurer's premiums-over-claims posture while dealing with a Tata AIG rejection, is a reminder that judicial patience with mechanical repudiation is thinning. Where hospitalisation itself went wrong rather than the insurance, the remedies run on a different track entirely: see our guide to medical negligence claims and forums.

Common mistake: arguing on the phone for six months. Phone calls do not exist, legally speaking. The claim that gets paid is the claim with a paper spine: the repudiation letter, your written grievance, the Bima Bharosa ticket, the Ombudsman filing. Two crisp written pages beat forty phone calls, and the two-year consumer limitation runs while you are on hold.

What to do this week if you are sitting on a rejection

- Pull out the repudiation letter; if you never received one in writing, demand it today by email.

- Diary two dates: two years from repudiation (consumer limitation) and one year from the insurer's final reply (Ombudsman window).

- Check the Section 45 arithmetic on a life policy: issuance, any revival, any rider, against the repudiation ground.

- On a health policy, map the stated ground against the policy's own definitions, waiting periods and the moratorium.

- Write once to the Grievance Redressal Officer, attaching the policy, the claim, and the repudiation, and asking for review with reasons.

- No satisfactory reply in 15 to 30 days: escalate to Bima Bharosa, then the Ombudsman or commission as the amount and conduct warrant.

A practice note on why insurers fold

Having handled these disputes, the pattern is unheroic: insurers price litigation risk, and a policyholder who demonstrates process discipline changes the price. A file that arrives at the Ombudsman with the repudiation letter, a reasoned grievance, the portal ticket and the policy's own clauses flagged reads like a file that will win at the commission with interest and costs added, and insurers settle those. The families who lose are almost never wrong on the law; they are unrepresented on paper. Build the paper. The system, for all its frustrations, genuinely rewards it: free forums the whole way to ₹50 lakh, a binding award at step five, and a commission at step six that has just shown, at ₹75 lakh, that it will enforce the statute against the largest insurers in the country.

Frequently Asked Questions

Can an insurer reject a life insurance claim after 3 years of the policy?

No. Section 45 bars questioning a life policy on any ground, including alleged fraud or non-disclosure, after three years from issuance, revival or rider addition, whichever is later. The NCDRC's July 2026 ₹75 lakh order against HDFC Life applied exactly this.

Does a revived policy restart the three-year window?

Yes. Revival gives the insurer a fresh three-year period from the revival date, which is the strongest practical reason to keep premiums from lapsing.

What is the time limit to challenge a claim rejection?

Two years from repudiation for the consumer commission, and approach the Insurance Ombudsman within one year of the insurer's final reply. Neither clock pauses for phone negotiations.

Is the Insurance Ombudsman's decision binding?

The award binds the insurer for complaints within its ₹50 lakh jurisdiction; the policyholder remains free to pursue other remedies if unsatisfied. The process is free and needs no lawyer.

What is Bima Bharosa?

IRDAI's online grievance portal. It registers your complaint with the regulator, routes it to the insurer for a time-bound response, and creates the official record later forums read.

Can a health claim be rejected for a pre-existing disease?

Only within the policy's defined PED terms and waiting periods, and never after the regulatory moratorium of continuous coverage except for proven fraud. Commissions require the condition to have been actually diagnosed, material and concealed.

The agent filled my proposal form incorrectly. Am I stuck?

Not necessarily; courts and forums have relieved policyholders where the insurer's own agent completed the form and the insured signed in good faith. But the safer course is always to complete the form yourself and keep a copy.

Should I accept the insurer's "ex gratia" partial offer?

Only with the numbers in front of you. Partial offers arrive precisely because the file looks strong; measure the offer against the claim plus interest and the realistic Ombudsman/commission timeline before signing any discharge voucher, and remember that a full-and-final discharge can end the claim.

This article is for general informational purposes only and does not constitute legal advice. Specific situations need specific counsel.