A Section 138 defence is never about denying that the cheque bounced. It is about attacking one of the legal pillars the complaint stands on: the existence of a legally enforceable debt, the validity of the demand notice, the identity of the persons dragged into court, or the maintainability of the complaint itself. Courts across India acquitted or quashed in at least four cheque bounce matters in five weeks this summer, and each ruling maps a pillar that gave way. This guide examines the six defences that genuinely work, anchors each to a 2026 decision or a settled Supreme Court authority, and explains the evidentiary standard an accused must actually meet, which is far lower than most accused believe and far higher than "I don't remember signing it".

Key takeaway: the Section 139 presumption means the accused starts the trial losing. But the presumption is rebuttable on a mere preponderance of probabilities, often from the complainant's own documents, and complaints that are defective on part-payments, notice, or party selection keep dying on their own procedural swords.

Start here: the presumption you are fighting

Under Section 139 of the NI Act, once the accused's signature on the cheque is admitted or proved, the court must presume the cheque was issued for the discharge of a legally enforceable debt or liability. Rangappa v. Sri Mohan, (2010) 11 SCC 441 settled that this presumption covers the very existence of the debt, not merely its discharge. The consequences:

- The accused bears the burden of rebutting the presumption, but only on the preponderance of probabilities, the civil standard, not proof beyond reasonable doubt.

- The accused need not enter the witness box or lead his own evidence at all; he can rebut the presumption from the complainant's own materials: the complainant's admissions in cross-examination, his income tax returns, his bank statements, the improbabilities in his story.

- A bare denial or a bald "the cheque was stolen" without supporting probability does nothing. The defence must make an alternative account more probable than not.

Every defence below is, at bottom, a way of making the complaint's story less probable than the defence's, or of showing the complaint never satisfied the statute in the first place.

Defence 1: part-payments not endorsed on the cheque

Where the drawer has repaid part of the debt before the cheque is presented, the instrument cannot be presented for the full original amount. Section 56 of the NI Act contemplates endorsement of part-payment on the instrument, and the Supreme Court in Dashratbhai Trikambhai Patel v. Hitesh Mahendrabhai Patel, (2023) 1 SCC 578 held that a cheque presented for the full amount after part-payment, without endorsement, does not attract Section 138 for want of a legally enforceable debt to that extent. The Kerala High Court applied the principle in July 2026, holding a complaint that concealed part-payments not maintainable.

How it runs in practice: the defence proves the payments (bank transfers are best; even the complainant's ledger will do), shows the cheque amount no longer matched the outstanding debt on the date of presentation, and the complaint collapses on maintainability rather than merits. For complainants the lesson is symmetric: disclose every rupee received and adjust the demand, or lose an otherwise good case.

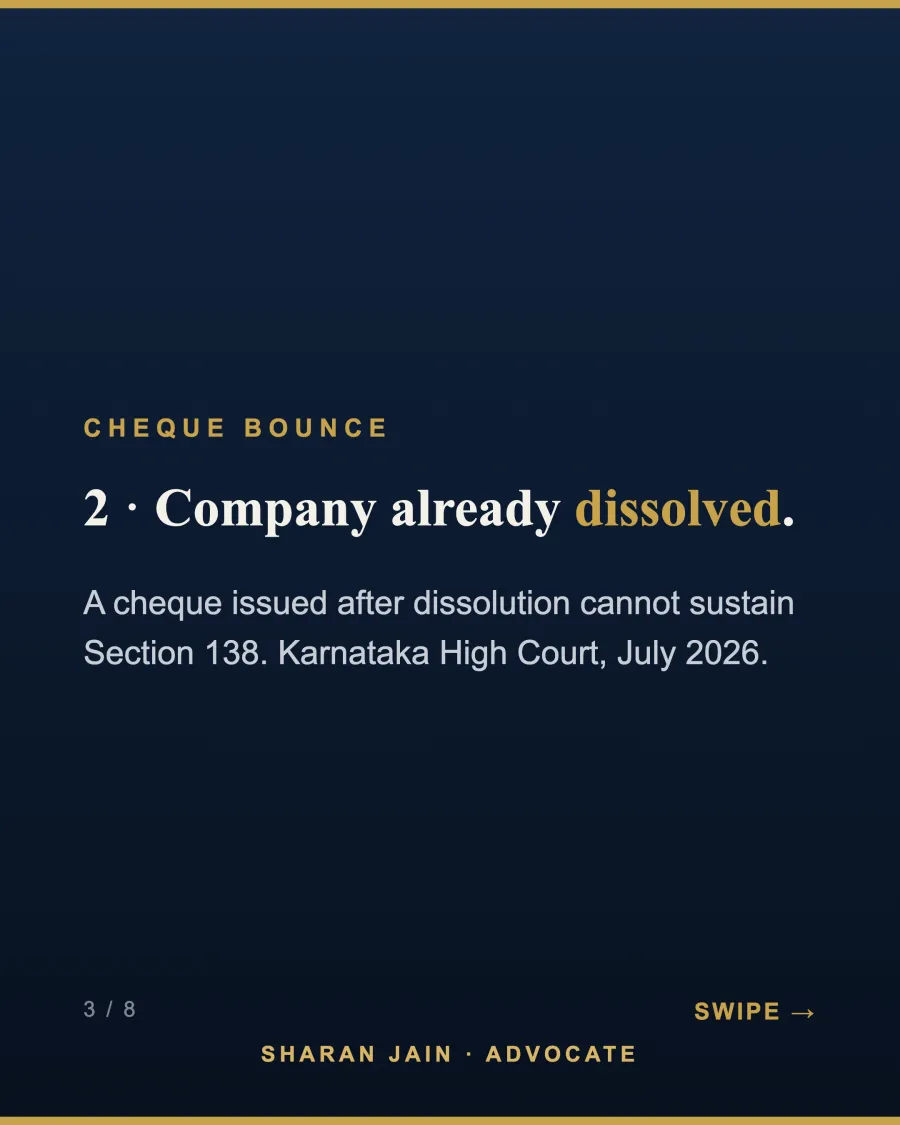

Defence 2: the company no longer existed

The Karnataka High Court quashed proceedings in July 2026 where the cheque had been issued after the company stood dissolved. A dissolved company is legally dead: it can neither commit the offence nor stand trial, and with no principal offender there is nothing for the vicarious liability of directors under Section 141 to attach to. Related variants of this defence include cheques signed after the drawer's account was demonstrably closed with the complainant's knowledge as part of a different arrangement, and complaints filed against companies already struck off the register. The status of the drawer entity on the date of the cheque and the date of presentation is the first document check any defence lawyer should run.

Defence 3: director in name only

Section 141 extends liability for a company's cheque to every person who, at the time of the offence, was responsible to the company for the conduct of its business, and to signatories. It does not extend to every name on the board. The Supreme Court's S.M.S. Pharmaceuticals v. Neeta Bhalla, (2005) 8 SCC 89 line requires the complaint to make specific averments of the accused's role; a high court reiterated in July 2026 that a bare designation is not an averment. Non-executive directors, nominee directors, and directors who resigned before the cheque was issued (with Form DIR-12 to prove it) keep winning quashing petitions on exactly this ground.

This defence is large enough to deserve its own map: our companion guide to directors' liability in cheque bounce cases under Section 141 covers the averment rules, the resignation defence, and the complainant's counter-playbook in detail.

Defence 4: a bond is not a debt

A Bengaluru sessions court acquitted an employee in June 2026 who had been prosecuted over a cheque taken against an employment bond, holding that treating the bond amount as a "debt" without establishing actual loss is impermissible under Section 138. The principle reaches far beyond employment: Section 138 requires a legally enforceable debt or other liability in existence when the cheque is presented. An unadjudicated damages claim is not that. Liquidated damages under Section 74 of the Contract Act still require proof of reasonable loss; a bond figure is a ceiling, not an entitlement. Security cheques generally follow the same logic: a cheque given as security converts into Section 138 territory only when a crystallised, due-and-payable liability exists at presentation, which is a question of the underlying transaction's documents.

Defence 5: no legally enforceable debt at all

The presumption is strong, but 2019's Basalingappa v. Mudibasappa, (2019) 5 SCC 418 shows how it breaks: where the complainant claimed to have lent ₹6 lakh in cash, the accused demonstrated from cross-examination that the complainant's declared income could not sustain such a loan, and the Supreme Court restored the acquittal. The recurring fact patterns that rebut the presumption:

- Financial incapacity of the complainant to have advanced the alleged cash loan (income tax returns, bank statements, admissions).

- Time-barred debts: a cheque for a debt already barred by limitation is not for a "legally enforceable" debt, subject to the fact-specific law on acknowledgment and fresh promises.

- Blank or misused cheques: handing over a signed blank cheque does not immunise the drawer (the filled amount is presumed authorised), but material alteration or filling contrary to an established arrangement, once made probable, defeats the presumption.

- Friendly or accommodation cheques with no underlying transaction, proved through the improbabilities of the complainant's own account.

Defence 6: a defective demand notice

The demand notice under Section 138(b) must be issued within 30 days of the return memo and must demand the cheque amount. An omnibus notice that lumps the cheque amount with other claims without itemising, or demands a different figure altogether, can be fatal; the Supreme Court's notice jurisprudence permits additional claims only when the cheque amount is separately and clearly demanded. Notices sent to a wrong address contrary to record, or complaints filed before the 15-day payment window expired, fail on the statute's own arithmetic. Every one of these dates is mapped in the standing guide to the cheque bounce case procedure under Section 138.

Common mistake (for the defence): saving every point for trial. Defects apparent on the face of the complaint, the dissolved company, the missing Section 141 averment, the omnibus notice, are quashing material under Section 482 BNSS/CrPC before the High Court, and taking them early can end the case years sooner. Points that need evidence, financial incapacity, part-payment, the security arrangement, belong at trial. Sorting your defences into these two buckets is the first strategic decision in every 138 brief.

The six defences at a glance

| Defence | Legal hook | 2026 authority / anchor | Route |

|---|---|---|---|

| Part-payment not endorsed | S.56 + "legally enforceable debt" | Kerala HC, July 2026; Dashratbhai Patel (SC) | Maintainability / trial |

| Company dissolved | No principal offender | Karnataka HC, July 2026 | Quashing |

| Director not in charge | S.141 averments | S.M.S. Pharmaceuticals (SC); HC, July 2026 | Quashing |

| Bond / security, no crystallised debt | "Debt or other liability" | Bengaluru sessions court, June 2026 | Trial |

| No enforceable debt | S.139 rebuttal | Rangappa; Basalingappa (SC) | Trial |

| Defective notice | S.138(b) proviso | Settled SC notice law | Quashing / trial |

A practice note on how these cases are actually won and lost

Two patterns repeat endlessly. On the defence side, cases are won in the complainant's cross-examination, not in the accused's evidence: the loan that outruns the lender's income, the ledger that shows the part-payment, the admission that the cheque was given in 2019 for a 2016 debt. Prepare the cross from the complainant's documents and most of the work is done. On the complainant's side, cases are lost to five minutes of carelessness at the start: an unendorsed part-payment, a notice that demands a padded figure, a complaint that names all seven directors because the master data was easy to download. None of this makes bouncing a cheque safe; where the debt is real and the paperwork clean, convictions remain the norm, as July's celebrity headlines showed. It makes carelessness unsafe, on both sides. And whichever side you are on, remember that settlement remains open at every stage; the economics are set out in our guide to cheque bounce settlement, compounding and Lok Adalat.

Frequently Asked Questions

What is the best defence in a cheque bounce case?

There is no universal best. The strongest defences attack a missing pillar: no legally enforceable debt (including part-payments not endorsed), a defective or late notice, absence of Section 141 responsibility, or a drawer entity that no longer existed. The right one depends on the documents.

Does the accused have to prove innocence beyond reasonable doubt?

No. The accused must rebut the Section 139 presumption only on a preponderance of probabilities, and may do so from the complainant's own evidence without stepping into the witness box.

Can a security cheque lead to conviction under Section 138?

Only if a crystallised, legally enforceable liability existed when the cheque was presented. Contingent or unadjudicated claims, like unproven bond amounts, do not qualify, as the Bengaluru acquittal of June 2026 illustrates.

Can a cheque bounce case be quashed before trial?

Yes, under Section 482 BNSS/CrPC where the complaint is unsustainable on its face: missing Section 141 averments, a dissolved company, an omnibus notice, or filing before the statutory windows expired.

Is a blank signed cheque a defence?

Generally no; filling an authorised blank cheque is presumed valid. The defence arises only where the accused makes it probable that the instrument was filled contrary to the arrangement or materially altered.

What if the debt was time-barred?

A cheque issued for a time-barred debt is not for a legally enforceable debt and cannot sustain Section 138, subject to the law on acknowledgments and fresh promises under the Limitation Act and Section 25(3) of the Contract Act.

Do these defences apply to the company's signatory too?

The signatory stands on a different footing from non-signatory directors: signing puts him presumptively in the net, and his defences are the substantive ones, debt, notice, part-payment, rather than the Section 141 averment defence.

If my defence fails, can I still settle?

Yes. The offence is compoundable at every stage, including appeal, though the Supreme Court's graded-costs framework makes late settlement progressively more expensive.

This article is for general informational purposes only and does not constitute legal advice. Specific situations need specific counsel.